Australian businesses are preparing for a major overhaul of the merger control regime under which they operate, with sweeping reforms set to come into play from January next year.

The changes, which passed through federal parliament in late 2024, are the most significant in more than 50 years and will shift the country from a voluntary merger notification system to what’s known as a mandatory and suspensory model.

At its core, the new regime aims to give the Australian Competition and Consumer Commission (ACCC) stronger oversight into M&A activity, ensuring deals are thoroughly investigated before they go live.

According to the ACCC, the new controls will promote fairness in the M&A market and protect consumers from deals that could harm prices or curb competition.

“The voluntary nature of the informal model meant some businesses were not notifying the ACCC about potentially anti-competitive transactions,” a spokesperson told Business News.

“And even if they did [notify us], we found businesses were completing, or threatening to complete, their merger transactions before the ACCC had time to finalise its review.”

According to advisers at law firm Hamilton Locke, between 1,000 and 1,500 mergers take place in Australia every year.

Of those deals, however, only about 350 are flagged with the ACCC for review.

The new legislation has made two major changes to rectify that.

The first update is the move to a mandatory model, which means businesses will be legally required to notify the ACCC before proceeding with certain mergers.

Under the current system, companies are not obliged to alert the regulator to deals that are in motion.

The second major shift is the suspensory rule, meaning once a merger is notified, it cannot be completed until the ACCC gives its formal approval.

This is markedly different from the current, informal approvals timeline, where deals can proceed even as the regulator rules on any competition concerns.

Of course, not every merger will fall under the new rules.

Technically speaking, companies must notify the ACCC if three conditions are met: the deal involves Australian operations; the merged group will have a combined turnover of more than $200 million; and either the target business or its assets generate over $50 million in Australian revenue, or the deal is valued above $250 million.

There are also new rules to govern very large mergers, as well as serial acquisitions (where several smaller transactions add up to harm competition) and supermarket deals (in the wake of last year’s ACCC inquiry).

Consequently, Hamilton Locke partner Deanna Carpenter said the regime’s financial thresholds would likely exclude any small-cap explorers considering a merger.

“But as you start to get into the mid-tier resources market, where we’ve seen a lot of activity lately, there will likely be implications,” Ms Carpenter told Business News.

Mid-market gold consolidation has dominated Western Australia’s corporate finance market in recent months, accounting for two of the top five M&A deals by value in the last six months, according to Data & Insights.

However, when asked how WA mining companies were preparing for the new merger controls, Ms Carpenter said she’d fielded disturbingly few enquiries.

“I think people are aware that this regime is coming, but they’re not across all the details,” she said.

“That is the job of the advisers, of course, but the key thing is making sure clients are aware early that, if they’re looking to acquire or be acquired, the new reforms may be a relevant factor.”

New hurdles

Spreading the word isn’t the only challenge the ACCC faces when it comes to rolling out new merger controls.

With a record number of companies slated to report, the watchdog’s workload is bound to multiply.

Whether it’s prepared for the influx in paperwork (and can keep approvals running on time) remains to be seen.

“The ACCC has no interest putting the kybosh on transactions that make sense, but the new reforms are bound to put more pressure [on the regulator],” Ms Carpenter said.

“If they’re not resourced adequately to handle that, it’s inevitable that there’ll be delays.”

The ACCC told Business News it was planning to hire 80 new staff in the coming years to handle the increased workload.

It was also building new IT systems to support the upsized reporting requirements, and to bring the agency in line with other regulators around the world.

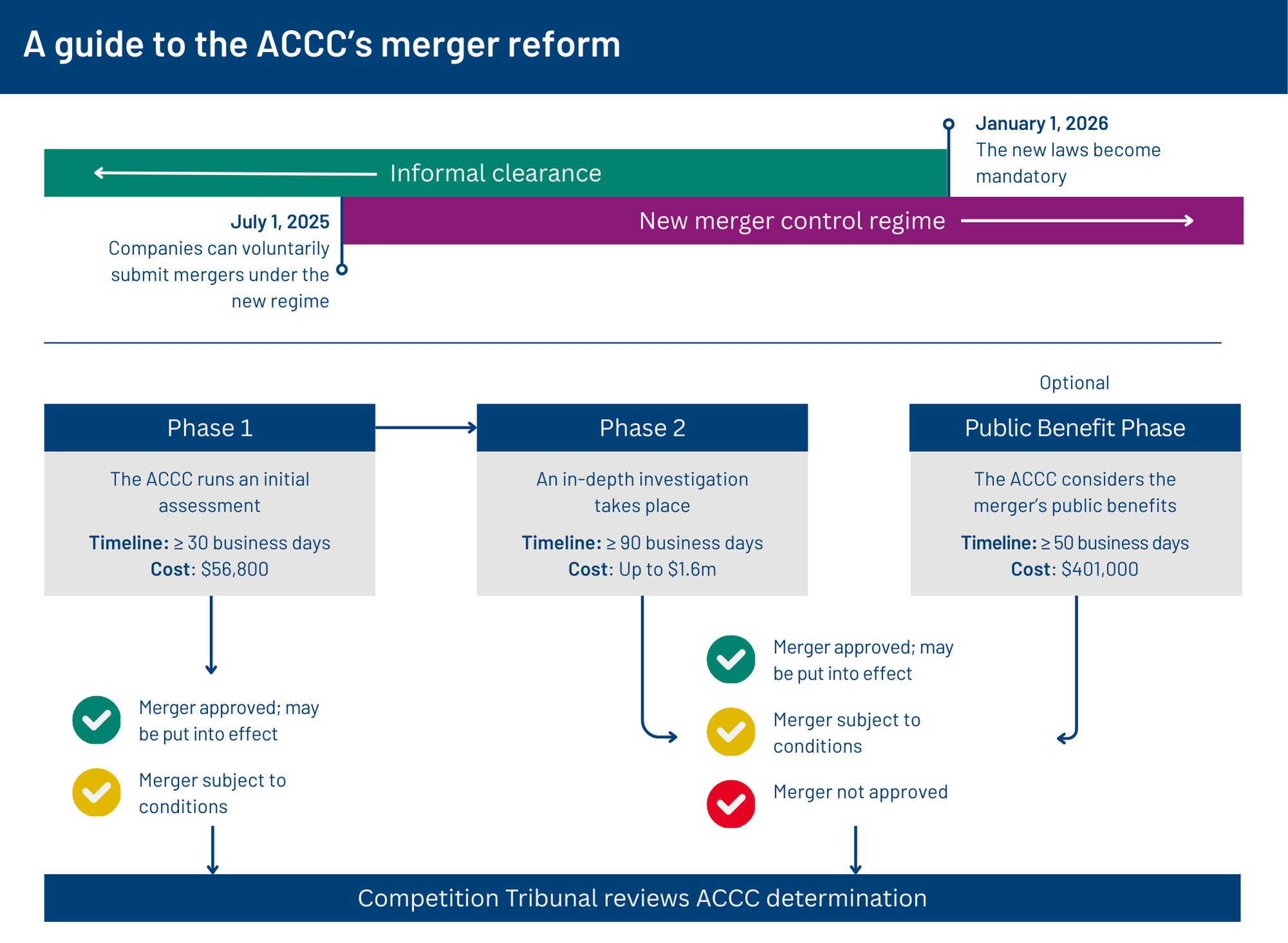

A multi-phase approvals timeline is also being rolled out to help businesses understand when they can expect deals to be rubber stamped.

Once companies flag mergers with the watchdog, they’ll enter an initial approvals phase that can last up to 30 business days.

The ACCC said it expected to make a call on 80 per cent of deals within 15 to 20 business days of being notified.

Then, if the merger passes muster, businesses will need to wait two weeks to move ahead with the deal so that applications can be lodged with the tribunal.

But if the ACCC needs to take a closer look at a merger, the process can move into phase two, which can involve up to 90 days assessing a transaction.

Businesses will need to pay close to $57,000 to flag their merger with the competition watchdog, and up to $1.6 million if the assessment moves to phase two (although there is a fee exemption available for small businesses).

Beyond the new approval timelines, advisers have raised questions over whether the merger regime will over-regulate transactions or even deter foreign investment.

In a note reflecting on the changing face of M&A, Allens partner Felicity McMahon said the proposed controls felt a little heavy handed.

“The ACCC currently sees more mergers per year than the European Commission, which is striking for a country with such a small population,” she wrote.

“The devil is in the detail, and my fear is that some of the benefits could be lost in [the regime’s] practical application.”

While the changes won’t be legally enforced until January 1 next year, the ACCC is giving businesses six months to acclimatise to the new reporting requirements.

Since the start of July, the competition watchdog has encouraged businesses to voluntarily flag their transactions.

One month in, the ACCC said it was yet to receive a formal notification under the regime, but that it had been engaging with a number of parties that were planning around the reforms.

“At this very early stage, the engagement has been around the level of information to provide when they notify an acquisition,” a spokesperson told Business News in late July.

“We expect the first merger notification to be lodged shortly.”

Other influences

It’s not just greater regulation changing the corporate finance landscape in 2025.

Shareholder activism and looming ESG requirements are also front of mind as companies navigate the evolving mergers market.

According to law firm Allens, Australia recorded a slight uptick in shareholder activism this year, with 56 companies targeted. This was slightly up from 54 in 2023.

Activists were also more successful in achieving their stated objectives, with a 25 per cent success rate in resolved campaigns compared with 16 per cent the year prior.

However, board-level influence is proving harder to secure. Just seven board seats were won by shareholder activists in 2024, down sharply from 26 in 2023.

Ms Carpenter said goldminer Capricorn Metals’ recent $180 million move for Warriedar Resources was a perfect example of shareholder activitism in action.

“I think it’s great that we’re seeing more shareholders using their voice in these transactions, although there are examples where it can be used for the wrong purposes,” she said.

Environmental considerations are also weighing on the deals space.

With Australia’s mandatory climate reporting regime set to begin in 2025 and ASIC cracking down on greenwashing, ESG is no longer a peripheral concern for companies aiming to transact.

At a recent advisory panel on mining and M&A held by Hamilton Locke, former De Grey Mining general counsel Sarah Standish said buyers were running the rule over ESG risks during the due diligence phase.

“There’s a lot more to consider during these transactions than just a target’s financial metrics,” she said.

“Digging into the status of native title and heritage agreements is something we’re seeing prioritised in the deal room.”

Getting acquainted

With so much change in the M&A space, the question becomes how companies should prepare to transact in an era of new regulation and shareholder activism.

David Southam, who serves on the boards of WA resources pundits Ramelius Resources, Cygnus Metals and Andean Silver, likened the current merger environment to a dating game.

“You need persistence in this space and it definitely takes stamina,” Mr Southam told advisers at the Hamilton Locke M&A panel.

“Sometimes the first date doesn’t quite work out, but both parties can go away and have time to reflect. Maybe they’ll get to a second date after all.”

According to Mr Southam, Ramelius has undertaken seven M&A transactions in the past seven years.

“We’re match fit, but we’ve got to remember we’re only one step away from a bad transaction,” he said.

Ms Carpenter also recommended companies lean on their advisers and ask the hard questions upfront to ensure potential mergers had the best chance at success.

“You need to be ready to have those tough conversations from the onset,” she said.

“It’s easy to get excited about the deal without talking through the dealbreakers and getting on the same page when it comes to valuation.

“The last thing you want is to spend valuable resources investigating a deal that just doesn’t pan out.”